Key Takeaways

Understand what is a credit report and how it influences loans, credit cards, rentals, and financial approvals.

Learn credit report components, what does a credit report contain, and how lenders interpret it.

Discover how to read a credit report step by step to spot mistakes and protect your credit profile.

Get practical guidance on how to check credit reports and dispute credit report errors effectively.

When lenders evaluate your financial background, they don’t just look at your credit score. They review your credit report. So, what is a credit report? A credit report is a detailed record of your credit history, including loans, payment behavior, and account activity.

Understanding what a credit report is essential because it forms the foundation of your credit score. According to the Federal Trade Commission (FTC), one in five consumers has an error on at least one credit report. That highlights the importance of credit report monitoring.

In this guide, we provide a clear credit report explained overview so you can understand what it contains and how to read it confidently.

What Is a Credit Report Meaning?

Let’s begin with credit report meaning in simple terms.

A credit report is a document compiled by credit bureaus that summarizes your credit activity. It does not assign a score, instead, it records the data used to calculate one.

There are three major credit bureaus in the United States:

Experian

Equifax

TransUnion

Each bureau may report slightly different credit report details depending on which lenders share information with them.

When asking what is a credit report, think of it as your financial history file. It tracks how responsibly you borrow and repay over time.

Understanding the difference between credit report and credit score is important. The report is the data. The score is the number derived from that data.

What Does a Credit Report Contain?

A key part of a credit report explained is knowing what a credit report contains.

Your credit report components typically include:

Personal Information: Name, address history, Social Security number (partial), employment information.

Account Information: Also known as your credit history report. Includes open and closed accounts, payment history, balances, and limits.

Public Records: Bankruptcies, tax liens, or civil judgments (if applicable).

Inquiries: Records of who has checked your credit. This includes hard inquiry vs soft inquiry distinctions.

Hard inquiries occur when you apply for credit and can affect your score. Soft inquiries, such as checking your own report, do not impact it.

Understanding these credit report sections explained helps you see what lenders evaluate before approving credit.

How to Read a Credit Report?

Learning how to read a credit report step by step prevents confusion.

First, review personal details for accuracy. Incorrect addresses or name variations can signal identity issues.

Second, examine account history carefully. Look for:

Late payments

Incorrect balances

Accounts you don’t recognize

Third, review inquiries. Multiple hard inquiries in a short period can raise red flags for lenders.

When learning how to read a credit report, focus on accuracy rather than emotion. Reports show factual history, not opinions.

Understanding credit report components allows you to interpret it with confidence.

Why is Credit Report Important?

The importance of credit reports goes beyond tracking debt.

Lenders use your credit report details to determine:

Loan eligibility

Interest rates

Credit limits

Rental approval

Insurance pricing

According to the Consumer Financial Protection Bureau (CFPB), negative information like late payments can remain on your credit report for up to seven years.

That’s why understanding what a credit report matters long-term. Errors or missed payments can affect financial opportunities for years.

A clean report strengthens financial flexibility.

How to Check Credit Report Safely?

Knowing how to check credit reports safely is essential.

Federal law allows you to access a free credit report from each bureau at least once per year. The official annual credit report website is:

https://www.annualcreditreport.com

This is the only government-authorized source for free reports.

Reviewing your report regularly helps detect identity theft and credit report errors early.

Monitoring supports the importance of credit report accuracy.

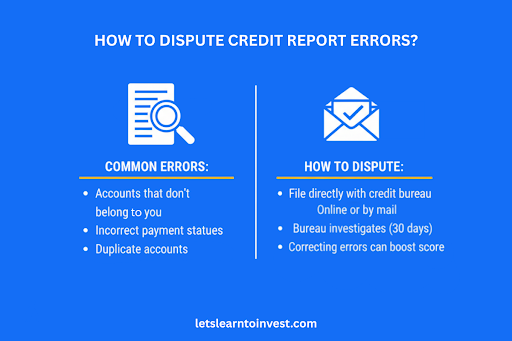

How to Dispute Credit Report Errors?

If you find mistakes, understanding how to dispute credit report errors is crucial.

Common credit report errors include:

Accounts that don’t belong to you

Incorrect payment statuses

Duplicate accounts

Outdated negative items

You can file disputes directly with the credit bureau online or by mail. The bureau typically has 30 days to investigate.

Correcting even one error can significantly impact your financial standing.

Understanding what a credit report is empowers you to maintain control over your financial record.

Final Thoughts

So, what is a credit report? It is a detailed record of your credit history that lenders use to evaluate financial reliability.

Understanding credit report meaning, what a credit report contains, and how to read a credit report gives you practical financial awareness. The importance of credit report monitoring lies in accuracy and prevention.

By reviewing your credit report components regularly and correcting credit report errors promptly, you strengthen your financial profile and protect future opportunities.

FAQs

1. What is a credit report in simple terms?

A credit report is a detailed record of your borrowing history, including accounts, payments, and inquiries.

2. How often should I check my credit report?

At least once per year, or more frequently if monitoring for identity theft or financial changes.

3. What does a credit report contain?

It includes personal information, account history, public records, and credit inquiries.

4. How do I get a free credit report?

Visit the official annual credit report website to access reports from all three bureaus.

5. Can I dispute errors on my credit report?

Yes. You can file disputes directly with credit bureaus, and they must investigate within 30 days.