Key takeaway

Fixed-income investments provide stable and predictable returns, making them ideal for risk-averse investors.

They help balance a portfolio by reducing overall risk during market volatility.

Options like government bonds, corporate bonds, FDs, and debt funds cater to different investor needs.

Even though they are safer, risks like inflation, interest rate changes, and credit default still exist.

These investments are best suited for beginners, retirees, and those seeking regular income.

In 2026, rising interest rates are making fixed-income instruments more attractive for investors.

Fixed-Income Investments: Everything You Need to Know in 2026

Introduction

In an era where financial markets are increasingly volatile, fixed-income investments have re-emerged as a cornerstone of smart portfolio construction. Whether you are a beginner seeking stability or an experienced investor looking to balance risk, fixed-income instruments offer predictability, income generation, and capital preservation.

As we move through 2026, global interest rate cycles, inflation trends, and economic uncertainties have made it more important than ever to understand how fixed-income investments truly work.

A Small Story to Begin With

Ravi, a 35-year-old salaried professional, had always invested in stocks. During a market downturn, he saw his portfolio drop by 25%. Frustrated, he spoke to a financial advisor who suggested allocating a portion of his money into fixed-income instruments.

Initially skeptical, Ravi invested in government bonds and debt mutual funds. Over the next year, while equities fluctuated wildly, his fixed-income portfolio provided steady returns and peace of mind.

That’s when Ravi realized wealth is not just about growth, but also about stability.

What Are Fixed-Income Investments?

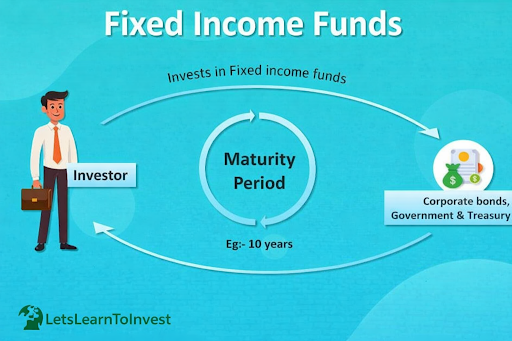

Fixed-income investments are financial instruments that provide regular and predictable returns in the form of interest or coupon payments. Unlike equities, where returns depend on market performance, fixed-income securities offer a predefined income stream.

At their core, these investments involve lending money to an entity such as a government or corporation in exchange for periodic interest payments and repayment of principal at maturity.

Common Types of Fixed-Income Investments

1. Government Bonds

These are issued by central or state governments and are considered the safest form of fixed-income investments.

Treasury Bills (T-Bills)

Government Securities (G-Secs)

Sovereign Gold Bonds

2. Corporate Bonds

Issued by companies to raise capital, these offer higher returns than government bonds but come with slightly higher risk.

3. Fixed Deposits (FDs)

A popular option in India, bank fixed deposits provide guaranteed returns with minimal risk.

4. Debt Mutual Funds

These funds invest in a mix of bonds and money market instruments, offering diversification and professional management.

5. Public Provident Fund (PPF)

A long-term government-backed scheme with tax benefits and stable returns.

How Do Fixed-Income Investments Work?

The concept is simple:

You invest (lend money)

You receive periodic interest

You get your principal back at maturity

For example, if you invest ₹1,00,000 in a bond with a 7% annual coupon, you will receive ₹7,000 annually until maturity.

Why Fixed-Income Investments Matter in 2026

1. Rising Interest Rate Cycles

With central banks adjusting rates globally, fixed-income instruments are offering more attractive yields.

2. Market Volatility

Equity markets continue to experience fluctuations due to geopolitical tensions and economic shifts.

3. Inflation Management

Certain fixed-income products are designed to counter inflation, helping preserve purchasing power.

Advantages of Fixed-Income Investments

Stable Returns: Predictable income stream

Lower Risk: Especially in government-backed securities

Capital Preservation: Ideal for conservative investors

Portfolio Diversification: Reduces overall volatility

Risks You Should Not Ignore

Even though fixed-income investments are considered safer, they are not risk-free.

1. Interest Rate Risk

When interest rates rise, bond prices fall.

2. Credit Risk

Corporate bonds carry the risk of default.

3. Inflation Risk

Returns may not keep up with rising prices.

4. Liquidity Risk

Some bonds may not be easily sold in the market.

Who Should Invest in Fixed-Income?

Conservative investors

Retirees seeking regular income

Beginners starting their investment journey

Investors looking to balance equity risk

Are fixed-income investments completely safe?

No investment is 100% risk-free. However, government bonds are among the safest options.

Can I lose money in bonds?

Yes, especially if interest rates rise or if the issuer defaults.

What is the ideal tenure for fixed-income investments?

It depends on your financial goals. Short-term for liquidity, long-term for stability.

Are fixed-income investments better than stocks?

Not better just different. They serve different purposes in a portfolio.

“Do not save what is left after spending, but spend what is left after saving.

— Warren Buffett

Common Mistakes to Avoid

Ignoring inflation impact

Investing without diversification

Chasing high yields without assessing risk

Not aligning investments with financial goals

How Beginners Can Start in 2026

Start with Fixed Deposits or PPF

Gradually explore debt mutual funds

Learn about bonds and yield concepts

Diversify across instruments

Future Outlook of Fixed-Income Investments

In 2026 and beyond, fixed-income markets are expected to evolve with:

Digital bond platforms

Increased retail participation

Better transparency in pricing

Innovative debt products

This makes it an exciting time for investors to explore fixed-income opportunities.

Final Thoughts

Fixed-income investments are not just about safety they are about financial discipline, stability, and balance. While equities may create wealth, fixed-income instruments protect it.

A well-structured portfolio is like a strong building equity provides growth, but fixed-income provides the foundation.

If you truly want to build long-term wealth, do not ignore the silent power of fixed-income investments.

FAQs

1. What is the safest fixed-income investment in India?

Government bonds and PPF are considered the safest options.

2. Can fixed-income investments beat inflation?

Some can, especially inflation-linked bonds and high-yield debt funds.

3. How much should I allocate to fixed-income?

Typically 20–50%, depending on your age and risk profile.

4. Are debt mutual funds better than fixed deposits?

They can offer better returns and tax efficiency, but come with slightly higher risk.

5. Is 2026 a good time to invest in bonds?

Yes, especially in a rising or stable interest rate environment.