Key Takeaways

Only 25% of Indians have emergency funds for unexpected situations.

75% of people remain financially vulnerable during job loss or medical emergencies.

Globally, 27% of adults have no emergency savings at all.

More than one-third of people carry higher credit card debt than their emergency savings.

Building an emergency fund is simple, but common mistakes weaken financial security.

Knowing what mistakes to avoid is as important as learning how to save.

A strong emergency fund should be liquid, accessible, and protected from impulsive spending.

The best emergency fund is not the biggest one it is the most reliable during crises.

Starting small is better than waiting for the “perfect” time to begin saving.

Saving early creates long-term financial stability and peace of mind.

A Story That Hit Close to Home

It was March 2020. Vikram, a 34-year-old marketing manager in Pune, believed he was financially secure. He had a mutual fund SIP, a term insurance plan, and even a recurring deposit. On paper, he looked financially disciplined.

But when the pandemic triggered salary cuts at his company, everything changed.

Within weeks, Vikram had to break his recurring deposit prematurely, redeem mutual funds during a market fall, and borrow money from his parents to manage daily expenses. The harsh reality was simple he never built an emergency fund.

For nearly two years, he had planned to start one. But like many people, he kept postponing it because other financial goals seemed more important.

Vikram’s story reflects the reality of millions of households. People invest, spend, and plan for the future but often ignore the one financial tool designed to protect them during uncertainty.

“An emergency fund is not a luxury. It is the price of financial peace.”

— Suze Orman

What the Data Tells Us

The statistics surrounding emergency savings are alarming.

According to Finology’s “India’s Money Habits” survey, nearly 75% of Indians do not have emergency funds and could struggle to pay EMIs during a sudden job loss. One out of every three Indians lacks both emergency savings and health insurance.

A survey conducted by Stable Money found that 47.38% of Indians have saved less than 10% of their required emergency corpus, while another 18.26% have saved only 10–20% of what they actually need.

Another 2024 survey covering over 1,700 respondents revealed that around 40% of people do not have sufficient emergency savings.

Globally, the situation is equally concerning. The Federal Reserve’s 2024 Survey of Household Economics and Decisionmaking reported that only 55% of adults in the United States had enough savings to cover three months of expenses. A Bankrate survey further showed that nearly 37% of Americans cannot handle a $400 emergency expense without borrowing or using credit.

The conclusion is clear: people understand the importance of emergency funds, but most fail to build them correctly.

Common Mistakes People Make While Building Emergency Funds

Mistake 1 Delaying Because the Amount Feels Too Small

One of the biggest mistakes people make is believing small savings do not matter.

Many individuals delay starting an emergency fund because they think ₹500 or ₹1,000 per month is insignificant. But financial security is built through consistency, not large one-time deposits.

A person saving ₹500 monthly still creates a ₹6,000 cushion within a year. That amount can cover medicines, groceries, fuel expenses, or temporary cash shortages.

The habit of saving matters more than the initial amount.

Financial experts in India generally recommend maintaining six to nine months of essential expenses in an emergency fund. However, reaching that number takes time, and every large corpus begins with a small first step.

The fix: Start immediately, even with a small contribution. Open a separate savings account and automate transfers into it every month.

Mistake 2 Keeping Emergency Funds in the Wrong Place

Another common mistake is storing emergency funds in unsuitable financial products.

Some people keep the money in their salary account, where it slowly disappears into routine spending. Others lock it in fixed deposits with withdrawal penalties or invest it in equity mutual funds that fluctuate with the market.

This defeats the entire purpose of an emergency fund.

An emergency fund must satisfy one essential condition: immediate accessibility without risk of capital loss.

During emergencies, people need liquidity not high returns.

Liquid mutual funds and dedicated savings accounts are often better alternatives because they provide accessibility along with relatively stable returns.

The fix: Keep emergency savings separate from daily-use accounts. Prioritise liquidity over returns.

Mistake 3 Using Emergency Funds for Non-Emergencies

A surprising number of people use emergency savings for non-essential spending.

Bankrate research revealed that while most withdrawals were for genuine necessities, around 19% were for non-essential expenses such as shopping, gadgets, or vacations.

This is dangerous because it creates the illusion of financial preparedness while silently weakening the safety net.

A genuine emergency includes situations like:

Job loss

Medical emergencies

Urgent home repairs

Critical vehicle repairs

Family emergencies

A discounted smartphone or a spontaneous vacation is not an emergency.

The fix: Clearly define what qualifies as an emergency before temptation arises. Written financial rules reduce impulsive decisions.

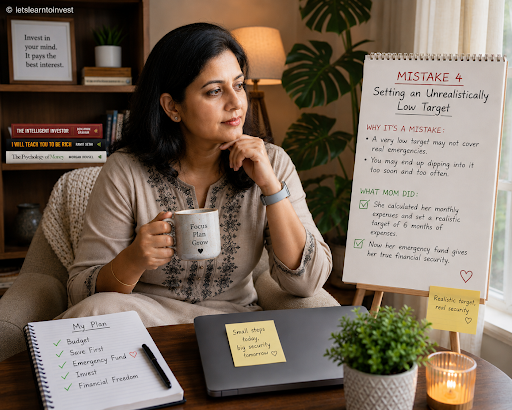

Mistake 4 Setting an Unrealistically Low Target

Many people underestimate how much emergency savings they actually need.

Three months of expenses may work for a salaried employee with stable income and no dependents. But freelancers, business owners, and single-income households face higher uncertainty and should ideally maintain six to twelve months of expenses.

In India, the absence of strong unemployment benefits increases the importance of maintaining a larger emergency cushion.

Medical inflation is also rising rapidly. A single hospitalisation can wipe out years of savings if proper insurance is missing.

The fix: Calculate essential monthly expenses carefully, including rent, EMIs, food, insurance, medicines, and utilities. Multiply this amount by at least six.

Mistake 5 Treating Investments as Emergency Funds

This is one of the most expensive financial mistakes.

People often assume that mutual funds, stocks, PPF balances, or insurance policies can function as emergency reserves. But investment products and emergency funds serve completely different purposes.

Equity markets can crash during economic downturns the exact period when people are most likely to lose jobs or face financial stress. Selling investments during a downturn locks in losses and damages long-term wealth creation.

Similarly, products like PPF and insurance policies have lock-ins or penalties that reduce flexibility during emergencies.

An emergency fund is not designed for growth. It is designed for protection.

The fix: Keep investments and emergency savings completely separate. Think of the emergency fund as financial insurance, not an investment vehicle.

Mistake 6 Not Automating Savings

Many people rely entirely on willpower to save money. Unfortunately, willpower is inconsistent.

At the end of every month, unexpected expenses appear, and emergency fund contributions get postponed repeatedly.

Automation solves this problem.

When money is transferred automatically on salary day, saving becomes non-negotiable. It removes emotional decision-making and builds discipline effortlessly.

The fix: Set up automatic bank transfers or recurring deposits immediately after salary credit.

Mistake 7 Ignoring Insurance While Building an Emergency Fund

Emergency funds and insurance work together.

Without adequate health insurance, a single medical emergency can destroy years of savings within days. In India, hospitalisation costs can easily range from ₹50,000 to several lakhs depending on the treatment.

Many households wrongly assume that emergency savings alone are enough.

But without insurance, even a strong emergency fund becomes vulnerable.

The fix: Build health insurance and emergency savings simultaneously. One protects the other.

Mistake 8 Failing to Rebuild After Using the Fund

Many people successfully use their emergency fund during a crisis but never rebuild it afterward.

Once the crisis passes, financial priorities shift back to lifestyle spending or investments, leaving the emergency reserve empty.

This creates a false sense of security.

An emergency fund only works when it is continuously maintained.

The fix: Replenish emergency savings immediately after using them. Treat rebuilding the fund as the highest financial priority.

How to Build an Emergency Fund the Right Way

Building an emergency fund does not require high income or advanced financial knowledge. It requires consistency.

Start by calculating your monthly essential expenses. Focus only on necessities like rent, food, utility bills, transportation, insurance premiums, and EMIs.

Next, decide your target amount. Most financial planners recommend maintaining at least six months of expenses.

Open a dedicated savings account or liquid fund exclusively for emergency savings. Avoid linking it to your daily spending account.

Automate monthly transfers into this account immediately after salary credit.

Review your emergency corpus annually because expenses increase over time.

Most importantly, protect your emergency fund from unnecessary withdrawals.

Final Thought

An emergency fund is more than money sitting in a bank account. It is peace of mind.

Financial emergencies are not rare events. Job losses, medical crises, economic slowdowns, and unexpected expenses are part of life. The difference between financial stability and financial stress often comes down to preparation.

The people who recover fastest from crises are not always the highest earners. They are the people who prepared before the crisis arrived.

Too many households wait for a “better income” or “better timing” before building emergency savings. But financial security begins with small, consistent action.

Even ₹200 saved regularly creates momentum.

The goal is not perfection. The goal is preparedness.

Your future self will thank you for the decision you make today.

“It is not about how much money you make. It is about how much money you keep.”

— Robert Kiyosaki

Frequently Asked Questions (FAQ)

Q1. How much emergency fund should I have in India?

Most financial experts recommend maintaining at least three to six months of essential expenses. Self-employed individuals or single-income families should ideally maintain six to twelve months of expenses.

Q2. Where should I keep my emergency fund?

Emergency funds should be stored in highly liquid and low-risk instruments such as dedicated savings accounts, sweep-in FDs, or liquid mutual funds.

Q3. Can mutual funds act as emergency funds?

No. Equity mutual funds fluctuate with market conditions and may lose value during economic downturns. Emergency funds must remain stable and accessible.

Q4. Should I build an emergency fund before investing?

Yes. Building an emergency fund should be the first financial priority before long-term investing because it prevents forced withdrawals during crises.

Q5. Can I use a credit card during emergencies instead of savings?

Credit cards provide temporary support but create debt with high interest costs. An emergency fund is always safer and cheaper than borrowing.

Q6. What qualifies as a genuine emergency?

A genuine emergency includes sudden job loss, medical expenses, urgent repairs, or unavoidable family crises. Luxury spending and vacations do not qualify.

Q7. How long does it take to build an emergency fund?

The timeline depends on income and savings rate. Consistency matters more than speed. Even small monthly contributions gradually create meaningful financial security.