Key Takeaway

Daily financial habits shape long-term wealth more than occasional big decisions.

Tracking expenses and controlling emotional spending improve financial discipline.

Consistent savings and regular investing help create financial security over time.

Learning about money daily strengthens decision-making and confidence.

Strong budgeting habits reduce stress and improve future financial planning.

Small disciplined actions repeated daily can completely transform financial life.

7 Daily Money Habits That Can Make You Financially Strong

A few years ago, a young office worker used to complain every month that his salary disappeared within days. He earned enough, but somehow savings never stayed in his bank account. One evening, his grandfather quietly asked him, “Do you control your money daily, or does money control you?” That question changed his life. He started tracking expenses, avoided impulsive shopping, and saved a small amount every day. Within a few years, he cleared debt, built investments, and became financially secure not because he earned crores, but because he built strong money habits.

“Financial freedom is available to those who learn about it and work for it.” Robert Kiyosaki

According to research published by the Federal Reserve and studies discussed by global financial education platforms, people who consistently follow disciplined saving and budgeting routines are far more likely to avoid debt stress and build long-term wealth. Small daily financial decisions often create bigger financial results than occasional large investments.

Why Daily Financial Habits Matter

Money management is not only about earning more. It is about developing consistent routines that protect and grow your wealth. Many people wait for a salary increase before improving finances, but strong financial discipline starts with simple daily actions.

This article works as a pillar guide covering essential habits, while each section also acts like a cluster topic connected to budgeting, savings, investing, and financial planning.

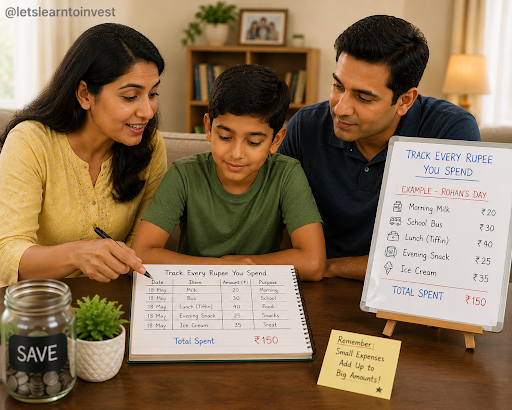

Track Every Rupee You Spend

One of the biggest reasons people struggle financially is that they never track where their money goes. Daily expense tracking creates awareness and helps identify unnecessary spending patterns. Whether it is online shopping, food delivery, subscriptions, or entertainment, small expenses silently damage savings.

Use a notebook, spreadsheet, or budgeting app to monitor spending daily. Reviewing expenses for just five minutes each evening can completely change your financial behavior. Over time, this practice develops stronger budgeting habits and smarter spending decisions.

People who track expenses regularly usually make better investment and saving choices because they understand their cash flow clearly.

Save Before Spending

Most people spend first and save whatever remains at the end of the month. Financially strong individuals reverse this process. They save first and spend later.

The best strategy is to automate savings immediately after receiving income. Even saving a small percentage consistently creates a powerful long-term effect. This habit builds emergency funds, reduces dependency on debt, and increases financial confidence.

Saving daily also teaches patience and delayed gratification, which are essential wealth building strategies.

Avoid Emotional Spending

Many purchases are emotional rather than necessary. Stress, boredom, social pressure, and online advertisements often trigger impulsive spending.

Before purchasing anything non-essential, pause and ask:

Do I truly need this?

Will this improve my life?

Can I wait 24 hours before buying it?

This simple pause can prevent unnecessary expenses. Financially disciplined people separate emotions from money decisions. They understand that temporary excitement should never damage long-term financial stability.

Read or Learn About Money Daily

Financial education is a lifelong process. Reading even one page about investing, taxation, budgeting, or savings daily improves financial thinking.

Many wealthy individuals dedicate time each day to learning about money. Knowledge helps people avoid scams, poor investments, and emotional financial decisions.

You do not need to study complex finance immediately. Start with basic concepts like emergency funds, SIPs, mutual funds, inflation, and debt management. Daily learning gradually improves decision-making confidence.

Use Cash Flow Planning

A strong financial life depends on understanding cash inflows and outflows. Cash flow planning ensures that income supports future goals rather than temporary desires.

Divide income into categories such as:

Essentials

Savings

Investments

Emergency fund

Lifestyle spending

This method creates balance and reduces financial stress. Smart money management tips often focus more on planning than earning because poor planning destroys even high salaries.

Review Financial Goals Regularly

Financial goals should not remain hidden in notebooks for years. Review them frequently to stay motivated and focused.

Your goals may include:

Buying a home

Building retirement savings

Starting a business

Becoming debt-free

Creating passive income

Daily reminders of these goals improve spending discipline. When people connect spending decisions with long-term dreams, they naturally become more financially responsible.

Invest Consistently Instead of Timing the Market

Many beginners wait for the “perfect time” to invest. Financially strong people focus on consistency rather than prediction.

Regular investing helps average market volatility and builds long-term wealth steadily. Even small investments made consistently can grow significantly through compounding.

Patience is often more important than timing in wealth creation. Daily financial habits combined with disciplined investing create long-term financial security.

How can someone start improving finances with a low salary?

A low salary does not stop financial growth if spending is controlled properly. Start by tracking every expense and identifying avoidable purchases. Build the habit of saving even a very small amount consistently because discipline matters more than amount initially. Focus on reducing wasteful spending rather than trying to appear wealthy socially. Improve skills regularly to increase future earning potential. Financial stability begins with habits, not income level alone.

Is daily budgeting really necessary?

Daily budgeting creates financial awareness and prevents overspending before it becomes dangerous. Many people underestimate how small expenses accumulate over time. Checking expenses daily keeps spending aligned with financial goals. It also reduces stress because you always know your financial position clearly. Budgeting is not about restricting life; it is about controlling money wisely. Consistency in budgeting often creates long-term financial confidence.

Why do people fail to save money consistently?

Most people fail because they treat savings as optional instead of essential. Emotional spending, lack of planning, and social pressure also reduce savings discipline. Another common reason is lifestyle inflation where expenses increase with income. Saving becomes easier when automated and connected to meaningful goals. Financially successful individuals prioritize future security over temporary luxury. Small consistent savings always outperform irregular large savings.

Should emergency funds be built before investing?

Yes, an emergency fund should usually come first because it creates financial protection during unexpected situations. Medical emergencies, job loss, or sudden expenses can force people into debt if no emergency savings exist. Ideally, maintain at least three to six months of essential expenses. Once this safety net is built, investing becomes less stressful and more disciplined. Emergency funds also prevent panic selling during market volatility. Financial security begins with protection before growth.

How can emotional spending be controlled?

Emotional spending can be reduced by identifying triggers such as stress, boredom, or peer pressure. Create a waiting period before making non-essential purchases. Avoid shopping when emotionally disturbed or frustrated. Maintaining financial goals visibly also helps reduce impulsive decisions. Many successful investors focus on long-term priorities instead of temporary satisfaction. Self-control in spending often creates more wealth than high income alone.

Is investing daily better than investing occasionally?

Consistent investing generally works better because it develops discipline and reduces market timing mistakes. Daily or regular investing benefits from rupee-cost averaging and long-term compounding. Occasional investing often becomes emotional and inconsistent. The key is maintaining regular contributions regardless of market conditions. Wealth creation usually rewards patience and consistency rather than short-term prediction. Even small regular investments can create substantial wealth over decades.

What financial habits should young adults focus on first?

Young adults should focus on budgeting, avoiding unnecessary debt, and building emergency savings first. Learning about investing early is also extremely valuable because time increases compounding benefits. Avoid lifestyle pressure created by social media and comparison culture. Developing strong saving habits in early years creates long-term advantages. Financial discipline built during youth often determines future wealth stability. Good habits started early become easier to maintain for life.

How important is financial education today?

Financial education has become essential because modern financial products are becoming increasingly complex. Without knowledge, people easily fall into debt traps, scams, or poor investment choices. Understanding taxes, inflation, investments, and savings improves financial independence. Financial literacy also increases confidence in decision-making. Even basic financial understanding can dramatically improve long-term wealth outcomes. Learning about money is now a life skill, not an optional subject.

Can small habits really create wealth?

Yes, wealth is often built through repeated small disciplined actions over long periods. Daily savings, consistent investing, careful budgeting, and controlled spending gradually create financial strength. Many financially successful people follow simple routines consistently rather than taking extreme risks. Small habits create powerful long-term financial results through compounding and discipline. Financial success rarely happens overnight. It usually grows quietly through daily consistency.

Final Thoughts

Financial strength is not reserved only for high earners or business owners. It is built by ordinary people who consistently make smart money decisions every single day. The difference between financial stress and financial freedom often comes down to habits rather than salary.

Start small. Track expenses today. Save a little tomorrow. Learn something new about money this week. These simple actions may look insignificant initially, but over time they create a financially secure and confident future.

FAQ

1.What are the best daily financial habits?

Tracking expenses, saving regularly, budgeting wisely, avoiding impulsive spending, and investing consistently are among the best daily financial habits.

2.How much should I save every month?

A common recommendation is saving at least 20% of income, but even smaller consistent savings can create strong financial growth over time.

3.Why is budgeting important?

Budgeting helps control spending, improves savings, reduces financial stress, and keeps money aligned with long-term goals.

4.Can financial habits improve wealth?

Yes, disciplined daily habits such as saving, investing, and careful spending can significantly improve long-term wealth creation.

5.What is the biggest mistake people make with money?

One of the biggest mistakes is spending without tracking expenses or planning future financial goals.

6.How can beginners start investing?

Beginners can start with SIPs, mutual funds, or basic diversified investments while continuing to learn about personal finance gradually.